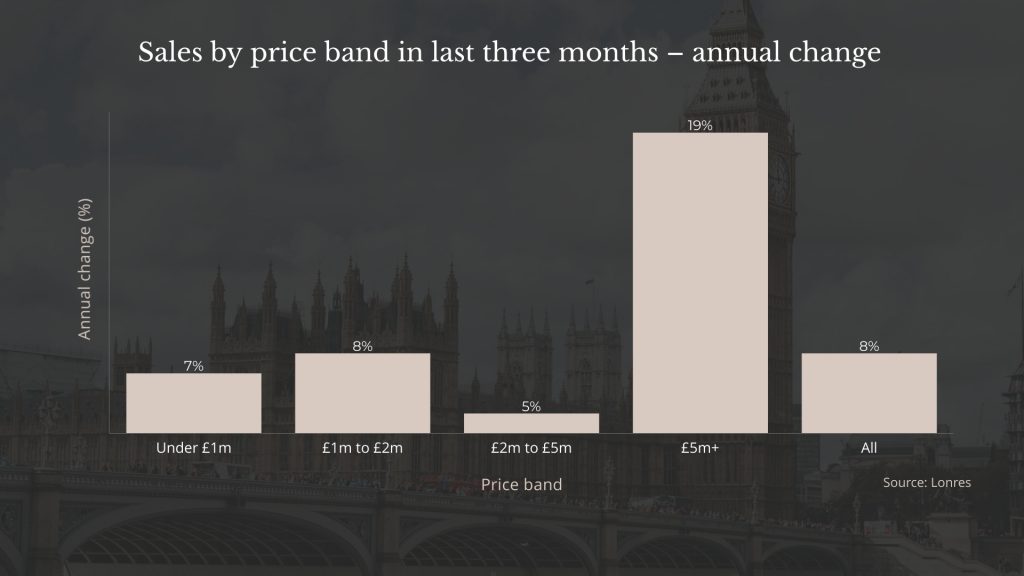

The London prime property market was as busy as it’s ever been over lockdown, but prices are still finding their feet.

+27.3%

Rise in number of properties sold compared with Q1 2020, just as the first lockdown hit.

18 Days

Properties are selling 18 days more quickly than this time last year.

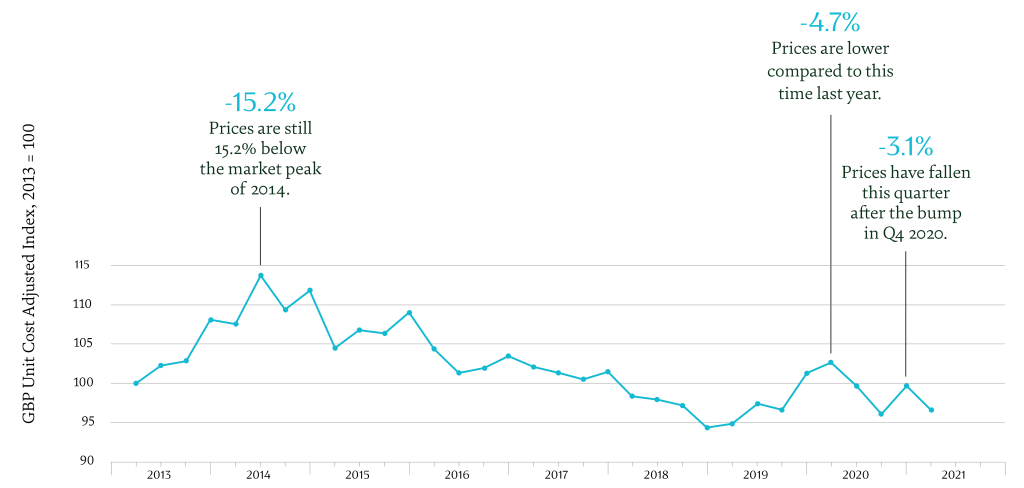

-4.7%

Fall in prices compared with same period last year.

Source: Coutts & Co, LonRes, April 2021

- With properties spending less time on the market compared to a year ago, sellers appeared to prioritise a quick sale rather than hold out for a higher price this quarter.

- Overseas buyers, an important source of demand for central London homes, have faced travel restrictions with fewer able to make the trip over to purchase or view prime property, which may also have impacted prices.

- Activity in the London prime property market continued to rise in Q1, despite the conditions of lockdown.

- The impending stamp duty holiday deadline on 31 March spurred on purchasers looking to take advantage of the savings. The deadline was extended in March, but by then many buyers were ready to complete.

- While the number of overseas buyers has been low due to travel restrictions, the arrival of a 2% stamp duty surcharge on overseas buyers at the end of March acted as an incentive for them to transact, too.

- New instructions were slow at the start of the quarter as many sellers assumed they’d left it too late to benefit from the influx of buyers hoping to meet the stamp duty holiday deadline and others were put off by lockdown. In March, the stamp duty extension and positive news on the easing of lockdown restrictions resulted in a surge in new instructions, making up for the slow months.

Prime Property Market Trends For 2021

Low Interest Rates Will Support Demand

The prospects for economic growth in 2021 have led to higher inflation expectations and rising bond yields (that is, falling prices). However, there’s no sign of any change in the Bank of England base rate in the UK. We continue to expect a very favourable low base rate regime for the next two to three years, which will continue to support demand for residential property.

Buyers And Sellers Emerge From Lockdown

As restrictions ease through the year, the previous ways of transacting are likely to re-establish themselves. We expect that this will see an increase in new listings as seller reluctance over viewings recedes. The real estate sector has done well to mitigate the barriers put up during lockdown, and some of these innovations – such as remote viewings – could stick, particularly for overseas buyers.

Return Of Overseas Buyers

We expect increased interest from overseas buyers as travel restrictions ease through 2021. Overseas interest in commercial property is already evident, reflecting an undervalued currency and attractive yields. Commercial estate agent Colliers reports that £3 billion was invested in UK commercial property in March, with overseas investors accounting for half of the assets. We expect trends in residential to follow commercial through 2021.